What Does P2P Lending Mean?

Whether you’re searching for the definition of peer to peer lending, curious about how it works, or just want to know what “P2P” actually means, you’re in the right place.

In this guide, we will break down everything you need to know about P2P lending.

Stick around, because by the end, you’ll know exactly how peer-to-peer lending platforms operate, what makes them different from banks, and how you can use them to meet your own financial goals.

What is P2P Lending?

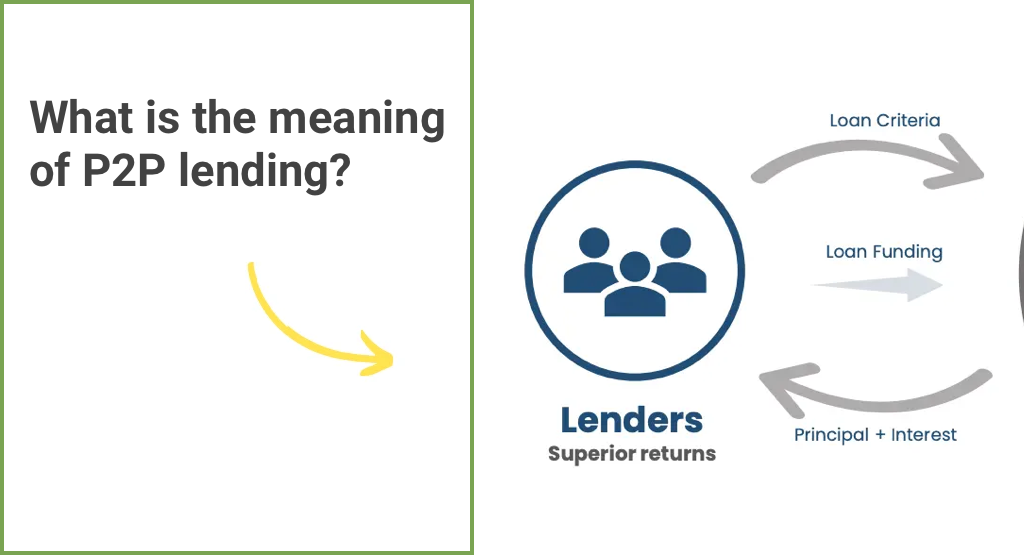

P2P lending (peer-to-peer lending) lets people lend and borrow money directly from each other through online platforms, skipping traditional banks entirely. This new way of doing finance creates a marketplace where those seeking better returns can meet those who are in need of money.

So what does P2P stand for? Simply “peer-to-peer,” emphasizing the direct, people-to-people nature of this model.

Unlike traditional banks that take deposits from savers to fund loans (pocketing the difference in interest rates), P2P platforms directly match people with money to those who need it.

The peer-to-peer lending definition boils down to this: it’s a financial matchmaking service powered by technology that benefits both sides of the transaction.

Borrowers often get more competitive rates and faster approvals, while lenders can earn returns that blow traditional savings accounts out of the water.

What makes the meaning of peer to peer lending truly revolutionary is how it democratizes finance. It opens doors for folks who might get overlooked by big banks while giving everyday investors access to an asset class that was once only available to financial institutio

The History and Evolution of P2P Lending

P2P lending is not actually a new concept – it started gaining traction around 2005 when the first platforms emerged.

Initially, these platforms focused on providing credit to people overlooked by banks and helping students consolidate loans at better rates.

Over the years, what began as a niche alternative has grown into a substantial financial sector.

The journey hasn’t always been so easy, have charted relatively unregulated waters. But things changed dramatically when regulators stepped in-especially in India where the RBI established clear guidelines for P2P lending.

Today’s RBI approved p2p lending companies operate with much greater transparency and security, making peer-to-peer lending explained more clearly to potential participants through standardized practices. This evolution has turned P2P lending from an experimental concept into a mainstream financial option that’s growing exponentially year after year.

How Does P2P Lending Work? The Process Explained

Let’s break down how does P2P lending work step by step:

Step 1 – Platform Registration

Both borrowers and lenders sign up on P2P platforms, creating profiles and verifying their identities. These platforms act as the digital marketplace where all transactions happen.

Step 2 – Borrower Application Process

Borrowers submit their loan requests, specifying how much they need and why they need it. They also provide financial information and supporting documents to establish their creditworthiness.

Step 3 – Risk Assessment and Credit Scoring

This is where the magic happens. P2P platforms don’t just take borrowers at their word-they dig deep.

Modern platforms assess over 600 different factors before green-lighting a loan. They check traditional credit scores but also analyze things like spending patterns, employment stability, and even digital footprints.

Based on this comprehensive evaluation, borrowers get assigned to risk categories that determine their interest rates.

Higher risk means higher rates-simple as that.

Step 4 – Loan Listing and Matching

Once approved, loan requests get listed on the platform where lenders can view them.

Each listing includes details about the loan amount, purpose, interest rate, and the borrower’s risk category.

Step 5 – Funding Process

Lenders browse through available loan listings and choose which ones to fund based on their risk appetite and return goals.

Many smart lenders spread their investments across dozens or even hundreds of different loans to minimize risk.

Step 6 – Money Transfer and Repayments

After a loan is fully funded, the platform transfers the money to the borrower’s bank account.

Borrowers then make regular payments (usually monthly) that include both principal and interest.

The platform collects these payments and distributes the appropriate amounts to all the lenders who funded that particular loan.

The entire peer to peer lending explained process shows how technology has made lending more accessible, transparent, and efficient for everyone involved.

What is a P2P Platform?

A P2P platform is a technology-driven online marketplace that directly connects individual lenders with borrowers, using advanced algorithms, digital verification, and secure transaction systems to manage the entire lending process.

These platforms use AI-powered risk assessment, automate credit profiling, and handle loan agreements, disbursal, and EMI collections digitally, ensuring fast, secure, and transparent transactions without traditional banks acting as intermediaries.

All fund transfers on a P2P platform are managed through regulated escrow accounts, enhancing security and compliance

These platforms serve several critical functions:

- User Verification: They verify the identities of both borrowers and lenders to prevent fraud.

- Credit Assessment: They evaluate borrowers’ creditworthiness using advanced algorithms and data analysis.

- Loan Administration: They handle all the paperwork, transfers, and ongoing management of loans.

- Collection Services: They manage the collection of repayments and the distribution of funds to lenders.

- Default Management: If borrowers fail to repay, platforms implement recovery procedures to protect lenders.

Different platforms may focus on specific types of loans. Some specialize in personal loans, while others focus on business financing, education loans, or even property investments. This specialization allows platforms to develop deep expertise in their particular niche.

Who Participates in P2P Lending? Lenders and Borrowers Explained

Let’s take a closer look at who’s who in the P2P lending ecosystem:

Borrowers: Who They Are and What They Seek

So what’s the borrowers meaning in the context of P2P lending?

Borrowers are individuals or businesses seeking funds for various purposes through P2P platforms instead of traditional financial institutions.

Typical borrowers include:

- Young professionals consolidating high-interest debt

- Small business owners seeking growth capital

- Individuals funding education, home improvements, or medical expenses

- Self-employed people who may not fit traditional banking criteria

These borrowers turn to P2P platforms because they offer:

- Potentially lower interest rates (especially for those with good credit)

- Faster application and approval processes

- More flexible terms

- Less stringent eligibility requirements than traditional banks

Each borrower gets categorized according to their risk profile, which directly affects their interest rate. This risk-based pricing ensures that lenders are compensated appropriately for the level of risk they take on.

Lenders: Who They Are and What They Seek

What’s the lender meaning in P2P? Lenders are individuals or entities who provide funds to borrowers through P2P platforms, essentially becoming individual bankers.

P2P lenders typically include:

- Retail investors looking for higher returns than traditional savings vehicles

- Professionals seeking to diversify their investment portfolios

- Early retirees looking for regular income streams

- Tech-savvy investors attracted to fintech innovations

The appeal for lenders includes:

- Higher potential returns compared to traditional fixed deposits or savings accounts

- The ability to start with small amounts (as low as ₹250 on some platforms)

- Portfolio diversification across multiple borrowers

- Greater control over where their money goes

- Regular monthly income from loan repayments

Unlike traditional banking where savers have no idea how their deposits are used, P2P lenders can choose exactly which loans to fund based on risk preferences, loan purposes, and other factors that matter to them.

The Booming P2P Lending Market: Growth and Trends

The P2P lending sector isn’t just growing-it’s exploding. Let’s look at some eye-opening statistics:

Global Market Growth

The P2P lending market has been on a remarkable trajectory:

- The global market size was valued at $190.43 billion in 2023

- It’s projected to reach $251.34 billion in 2025

- By 2029, it’s expected to hit a staggering $729.07 billion

- That represents a compound annual growth rate (CAGR) of 30.5%

These are not just impressive numbers – they represent a fundamental shift in how people access and provide financing around the world.

India’s P2P Lending Landscape

In India specifically, the market is showing exceptional growth potential:

- The Indian P2P lending market reached $7.53 billion in 2024

- It’s forecast to grow to $42.92 billion by 2033

- That’s a CAGR of 21.34% during 2025-2033

This growth is fueled by India’s rapid digitalization, with smartphone users exceeding 650 million and internet subscriptions surpassing 950 million by mid-2024.

What’s Driving This Growth?

Several powerful trends are propelling P2P lending forward:

- Technological Innovation: Fintech advances including AI, blockchain, and data analytics are making P2P platforms smarter, safer, and more user-friendly.

- Digital Adoption: The surge in smartphone usage and internet access has created a perfect environment for digital financial services to thrive.

- Favorable Regulations: Many countries have established clear regulatory frameworks for P2P lending, giving the industry legitimacy and consumer protection.

- Financial Inclusion Push: P2P lending helps bridge the credit gap for underserved populations that traditional banks often overlook.

- Attractive Economics: The model offers better rates for borrowers and higher returns for lenders compared to traditional banking-a win-win that fuels adoption.

These growth statistics and trends highlight just how significant P2P lending has become in the global financial ecosystem, moving from an alternative fringe option to a mainstream financial service.

The Benefits: Why People Choose P2P Lending

P2P lending offers compelling advantages for both sides of the transaction.

Let’s explore what makes it so attractive:

Advantages for Borrowers

- Competitive Interest Rates: Many borrowers-especially those with good credit-can access loans at rates lower than credit cards and sometimes even traditional bank loans.

- Speed and Convenience: The digital-first approach means borrowers can apply online in minutes and often receive funds within days-much faster than the weeks it might take at traditional banks.

- Accessibility: P2P platforms often approve borrowers who might get rejected by conventional banks, including those with limited credit history or non-traditional income sources.

- Transparency: Clear, upfront terms mean no hidden fees or surprise charges that often come with traditional loans.

- Fixed Repayment Terms: Most P2P loans come with fixed interest rates and predetermined repayment schedules, making budgeting straightforward.

Advantages for Lenders

- Higher Returns: This is the big one. While traditional fixed deposits might offer 7-9%, P2P platforms like LenDenClub have delivered returns up to 12%. That difference may seem small, but it adds up dramatically over time.

- Portfolio Diversification: By spreading money across many different loans, lenders can reduce risk while maintaining strong returns. Some platforms enable diversification down to just a few rupees per loan.

- Flexible Lending Amounts: You can start with as little as ₹250 on platforms like LenDenClub, making P2P lending accessible to almost anyone.

- Regular Income Stream: Monthly repayments provide a steady cash flow that many investors find attractive.

- Direct Control: Unlike mutual funds or stocks, P2P lending gives investors direct control over exactly where their money goes.

P2P vs. Traditional Banking: A Comparison

Feature | P2P Lending | Traditional Banking |

|---|---|---|

Interest Rates for Borrowers | Often lower, especially for prime borrowers | Generally higher due to overhead costs |

Returns for Lenders | Higher (9-12% typically) | Lower (3-7% for fixed deposits) |

Application Process | Fast, digital-first experience | Often lengthy with paperwork |

Approval Time | Often within 24-48 hours | Can take weeks |

Accessibility | More inclusive of varied financial profiles | Stricter criteria, often excludes many applicants |

Transparency | Clear fee structure and terms | Sometimes hidden fees and complex terms |

Customer Experience | Modern, tech-driven interface | Often bureaucratic and formal |

This comparison makes it clear why many people are adopting P2P lending as either borrowers or lenders – it simply offers better economics and experiences for both sides of the transaction in many cases.

Risks of P2P Lending

While the benefits are compelling, P2P lending isn’t without risks.

Let’s take an honest look at the potential downsides and how to manage them:

Risks for Lenders

- Default Risk: The biggest concern for lenders is that borrowers may fail to repay their loans. Unlike bank deposits, P2P investments typically aren’t protected by government guarantees like deposit insurance.

- Platform Risk: If the P2P platform itself experiences problems or shuts down, lenders might face difficulties managing their investments or recovering their funds.

- Liquidity Limitations: Most P2P investments are locked in for the loan term-usually months or years. Unlike stocks or mutual funds, you typically can’t sell quickly if you need your money back early.

- Potential Returns Volatility: Actual returns can fluctuate based on default rates, which may increase during economic downturns.

Risks for Borrowers

- Interest Rate Consideration: While P2P rates can be competitive, borrowers with lower credit scores might still face high interest rates.

- Privacy Implications: Borrowers must share substantial personal and financial information on the platform.

- Credit Score Impact: Late payments or defaults on P2P loans will damage credit scores just like any other loan.

Smart Risk Management Strategies

For Lenders:

- Diversify Aggressively: Never put all your money in one or even a few loans. Spread investments across hundreds of different loans to minimize the impact of any single default. Platforms like LenDenClub offer automated diversification tools that can spread your investment across thousands of borrowers with just a few clicks.

- Start Small: Begin with a small amount to understand the platform and process before committing larger sums.

- Choose Established Platforms: Stick with regulated, well-established platforms that have strong track records and proper regulatory approvals.

- Understand Risk Grades: Pay attention to borrower risk categories and adjust your portfolio mix according to your risk tolerance.

- Only Invest “Patient Money”: Don’t put in funds you might need in the short term, as P2P investments are generally not liquid.

For Borrowers:

- Borrow Responsibly: Only take what you genuinely need and can comfortably repay.

- Compare Multiple Platforms: Interest rates and terms can vary significantly between platforms.

- Read Terms Carefully: Understand all fees, penalties, and repayment requirements before accepting a loan.

By implementing these risk management strategies, both lenders and borrowers can navigate P2P lending more safely while still enjoying its many benefits.

P2P Lending Regulations: Protection and Oversight

The regulatory landscape for P2P lending has evolved significantly, adding crucial protection for participants.

Here’s what you should know:

RBI Regulations in India

In India, the Reserve Bank of India (RBI) has established a comprehensive regulatory framework for P2P lending:

- NBFC-P2P Classification: All P2P lending platforms must register as Non-Banking Financial Companies (NBFC-P2P) and obtain certification from the RBI.

- Investment and Borrowing Limits:

- Lenders can invest a maximum of ₹50 lakh across all P2P platforms

- Borrowers can borrow up to ₹10 lakh across all platforms

- A single lender cannot lend more than ₹50,000 to the same borrower

- Fund Security: Platforms must establish separate escrow accounts for funds from lenders and borrowers, managed by bank-promoted trustee companies.

- Transparency Requirements: Platforms must clearly disclose their loan selection process, fees, and risk assessment methodology.

- Prohibited Activities: P2P platforms cannot provide credit guarantees, facilitate secured loans, cross-sell products except loan-specific insurance, or enable international fund transfers.

These regulations have significantly strengthened trust in P2P lending by providing clear rules and protections for all participants.

How Regulations Benefit You?

Whether you’re a borrower or lender, these regulations offer important protections:

- Platform Stability: Regulatory requirements ensure platforms have adequate capital and sound business practices.

- Transparency: Mandated disclosures help you make informed decisions.

- Fund Security: Escrow requirements protect your money from platform insolvency.

- Risk Management: Lending limits prevent excessive concentration of risk.

- Grievance Redressal: Regulated platforms must have formal processes for addressing complaints.

As the industry continues to mature, these frameworks will likely continue to evolve, balancing innovation with consumer protection.

How to Get Started with P2P Lending?

Whether you’re interested in borrowing or lending, here’s how to get started with P2P lending:

For Borrowers: Your Path to Funding

- Research Platforms: Compare interest rates, loan terms, processing times, and user reviews across multiple P2P platforms. Make sure they’re registered with the RBI.

- Complete Registration: Register for an account on the platform of your choice, complete KYC with the required documents (PAN, Aadhaar etc) and add your bank account details.

- Documentation Preparation: Just get all your documents ready which includes your income documents, bank statements, identity proofs.

- Apply for Your Loan: Say how much you’re looking to borrow, what you need it for and over how long. Be honest and complete your submission.

- Credit Assessment: The company will check your credit by looking at traditional and alternative factors. This can involve reviewing your credit score or report, examining your bank history and employment record.

- Review Your Offer: If approved, you’ll receive a loan offer with specific terms and interest rate. Review all details carefully before accepting.

- Receive Funding: Once your loan is funded by lenders, the money will be transferred to your bank account. Depending on the platform, this can happen within a few days or even hours.

- Manage Repayments: Set up automatic payments to ensure you never miss a due date. Timely repayments will help build your credit score and history on the platform.

For Lenders: Your Investment Journey

- Educate Yourself: Know the ins and outs P2P borrowing, potential returns and risks. Staying well-informed is your best protection.

- Pick a Trustworthy Platform: Opt for a platform that is RBI-registered, has a solid history, and operates with transparency. Read reviews and compare their default rates.

- Set Up Your Account: Register, verify, and connect your bank account.

- Develop an Investment Strategy: Decide how much you want to invest, your risk tolerance, and whether you prefer manual or automated investing. Consider starting with a small amount as you learn the ropes.

- Fund Your Account: Transfer money from your bank to the P2P platform.

- Start Investing: Choose individual loans manually according to your preferences, or take advantage of auto-investment tools to diversify your investment in many loans. Try to put your money into at least 100 different loans to mitigate risk.

- Keep an Eye on Performance: Keep an eye on the dashboard as you would if you lent money to a friend – this way you can see repayments, returns and whether there are any late payments or defaults.

- Reinvest Returns: For compounded growth, consider reinvesting your returns into new loans rather than withdrawing them.

The Future of P2P Lending: What’s Next?

The P2P lending industry continues to evolve rapidly. Here’s what to watch for in the coming years:

Emerging Technologies Reshaping P2P

- Integration with Blockchain: Blockchain can potentially add more transparency and security to P2P transactions. Lending agreements might be able to be fully automated through smart contracts, which would bring a new level of efficiency.

- AI-Powered Risk Assessment: Artificial intelligence is growing more sophisticated at predicting borrower behavior than merely relying on conventional credit scores. These systems take into account thousands of data points to make lending more precise.

- Open Banking Connections: Direct access to banking data (with permission) allows for real-time financial assessment and seamless fund transfers, streamlining the entire lending process.

- Mobile-First Experiences: As smartphone penetration continues to grow, especially in emerging markets, P2P platforms are focusing on mobile-optimized experiences that allow users to manage lending and borrowing on the go.

Market Trends to Watch

- Industry Consolidation: The market is likely to see consolidation as larger, well-established platforms gain market share and smaller players merge or exit.

- Institutional Participation: More institutional investors are entering the P2P space, bringing greater capital and stability to the ecosystem.

- Specialized Niche Platforms: We’re seeing a proliferation of platforms targeting specialized loan types or borrower segments, such as student loans, healthcare financing, or green energy projects.

- Cross border growth – As legislation becomes more developed, there is a potentially large opportunity for p2p lending to lend across borders creating new opportunities for both borrowers and investors.

As P2P lending evolves, the platforms that succeed will be those that can balance innovation with risk management, regulatory compliance, and exceptional user experience.

For participants in this dynamic marketplace, staying informed about industry developments will be key to making the most of the opportunities ahead.

Conclusion

Peer-to-peer lending is a fundamental shift in how money moves between people who have money and people who need money.

So, regardless of whether you want to lend money for your next venture or earn more interest on your savings, P2P lending presents some exciting prospects that are at least worth looking into.

There is only one key to success in this space – knowledge, strategic planning, and a realistic view of both opportunities and risks.

The future of finance is becoming more direct, more accessible, and more personal

Peer-to-peer lending isn’t just part of that future—it is putting the industry at the forefront.

Team LenDenClub

LenDenClub is India’s largest alternate investment platform which started operations in India in 2015. We have been helping investors diversify their investments beyond traditional investment instruments ever since.